Weather: Dry Pattern Driving Early Season Risk Premium

16 April 2026

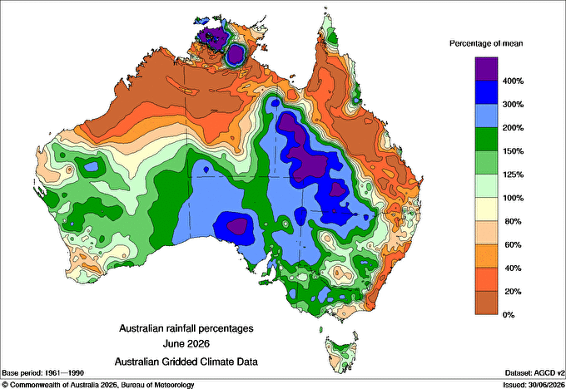

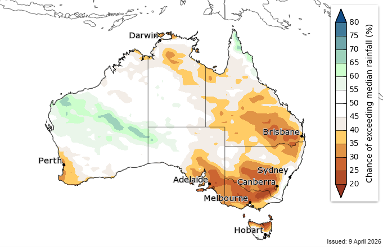

Seasonal conditions across Northern growing regions continue to deteriorate. Large parts of Northern NSW and Southern QLD experienced below average rainfall through late summer and early autumn, and there is no meaningful improvement in the current forecasts.

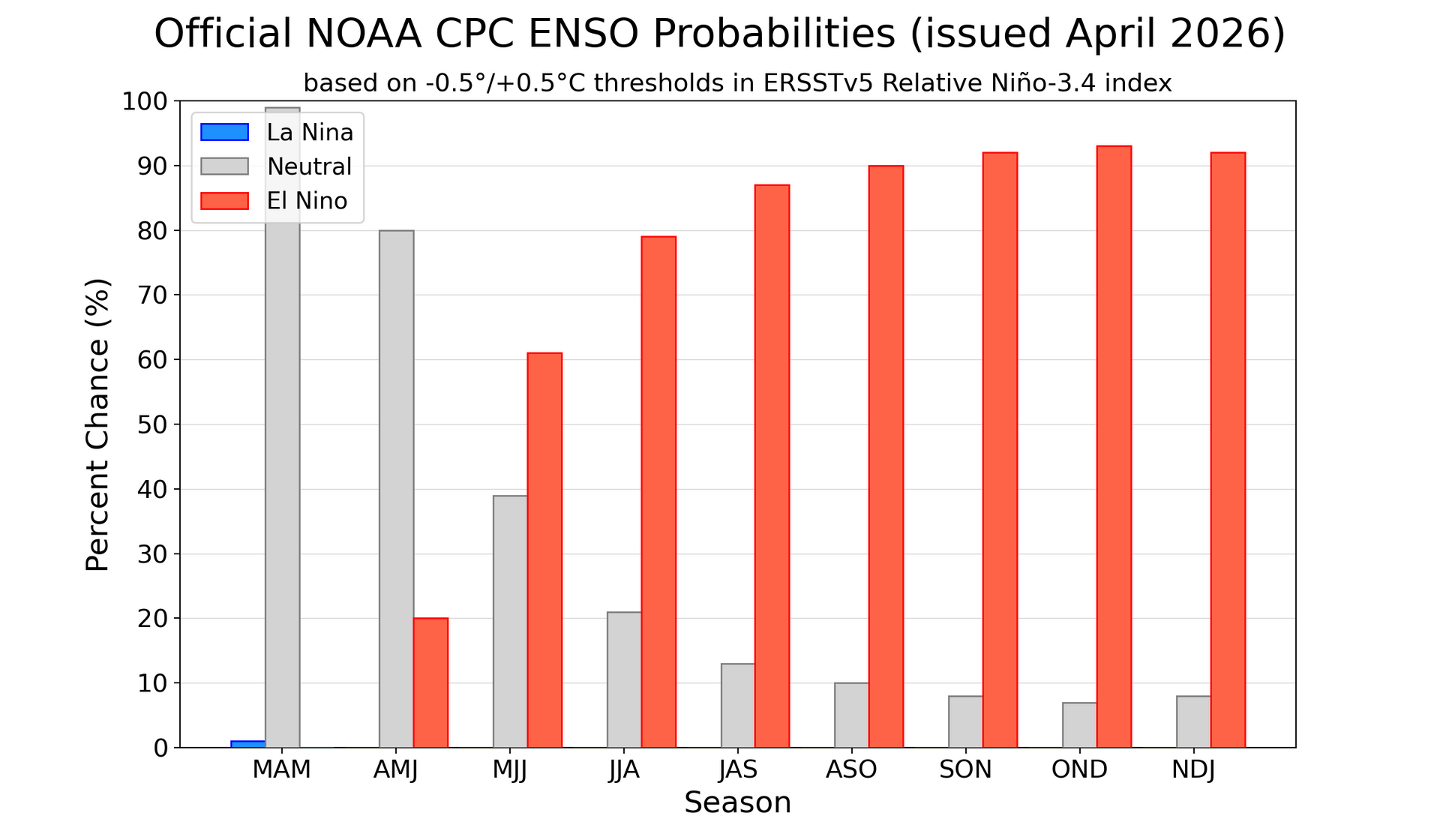

The Bureau of Meteorology’s most recent long-range outlook continues to point to a drier and warmer than average pattern across Eastern Australia. All major global models, including the BOM, continue to show rapid warming across the tropical Pacific over coming months. Neutral ENSO conditions are expected to persist through late autumn, before a speedy transition into an El Niño phase by mid-winter.

Source: https://cpc.ncep.noaa.gov/products/analysis_monitoring/enso/roni/probabilities.php

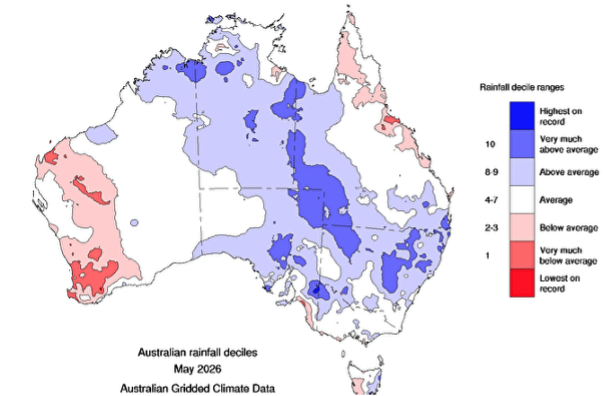

Rainfall - chance of above median for May to July.

Source: https://www.bom.gov.au/climate/outlooks/#/rainfall/median/seasonal/0

The dry weather pattern is now clearly being reflected in the paddock, with soil moisture profiles becoming depleted in the North East as we move deeper into the 2026/27 planting window. The market has responded accordingly, with a sharp rally in domestic bids across both wheat and barley in northern zones for both old and new crop.

Southern markets have followed the north higher, albeit at a more measured pace. South Australia and Western Australia and parts of Victoria have benefited from solid rainfall to start 2026 and currently have a solid soil moisture profile heading into sowing.

Domestic logistics and consumer drawing arcs will remain the key focus for northern markets in the near term, as exports out of Northern NSW and QLD are effectively priced out of new demand. The premiums being built into northern values are now doing the job of incentivising grain movements and gradually extending draw arcs into southern zones. Similar conditions were seen through the 2018/19 season, when a significant production deficit in the northeast resulted in grain being drawn from South Australia and Western Australia, with material volumes moved via road, rail and sea into Queensland to meet feedlot demand. That inter-state flow ultimately reset domestic price relationships and opened WA and SA up as the supply source into northern feed markets alongside traditional export programs. We are not at that point yet and the season has time to improve and restore balance, but the supply chain is in place and will respond quickly if the season continues to deteriorate.

The Global Picture

The latest update from the USDA has painted a neutral to bearish tone on global supplies.

Global feed grain production was revised slightly higher, with gains in South Africa, Russia and the EU. Demand also lifted modestly, led by feed use, resulting in a small increase in ending stocks and a broadly comfortable supply outlook. Argentina remains one to watch, with a wide 15 million tonne gap between USDA and Rosario corn production estimates.

In wheat, supply changes were minor, however a sharp reduction in India’s domestic consumption lifted global stocks to multi-year highs. Much of this sits within India and China and is unlikely to impact export flows unless the Indian market builds a large export program.

Attention is turning to spring weather in the northern hemispher. Russian conditions have improved following solid winter snowfall, although earlier dryness and the need for timely spring rains mean some production risk remains. Similarly in the US, HRW conditions across the US Southern Plains are varied, with parts of the central and southern belt still carrying a moisture deficit despite some recent improvements. SRW areas are in better shape overall, with adequate soil moisture across much of the Midwest supporting a solid start to spring growth, although there are still a few drier pockets to watch.

Globally, growers are facing a similar set of challenges to those in Australia. Elevated input costs, particularly fuel and fertiliser, continue to pressure margins even with supportive grain prices. Producers in key exporting regions are being forced into more disciplined decision making, with a greater focus on input efficiency, crop mix and overall risk. This is likely to influence planting intentions, particularly in higher cost or lower yielding areas. As a result, if global grain balance sheets tighten, the market may need to incentivise prodution through a boost to prices and margins.

The Overall Washup

Dry weather across northern Australia is driving early season risk premium and strengthening local pricing, while global markets remain suitably supplied. Producers are dealing with elevated input costs, keeping margins under pressure both locally and abroad, reinforcing the importance of decision making both when the crop goes in and when the crop gets sold.

While the season still has time to improve in Australia, current weather models alongside continued global conflicts, suggest volatility will remain elevated with opportunities likely to arise for growers and pool managers who are proactive in managing both production and pricing risk respectively. As always, if you need assistance with grain marketing, please contact your local Advantage representative or call head office on 1300 245 586. Fingers crossed for some rain and diesel and best of luck for the season ahead.

Share This Article

Other articles you may like